Khalifa University professor teams with industry pros

and Nobel laureate to improve strategy›››

Technology

Blockchain might be the most hyped technology relatively few people understand or actively use.

Its earliest and perhaps most famous use – the cryptocurrency bitcoin – has become a household word, with other digital-currency companies such as Ethereum and Cardano gaining traction in the public consciousness and with investors.

Despite wild price volatility and scams that the United States’ Federal Trade Commission says cost 7,000 people more than US $80 million between October 2020 and March 31, 2021, the crypto economy keeps rolling along, with market capitalization topping $2.4 trillion in May 2021, up from around $200 billion in 2019. And according to a 2021 Fidelity study, seven in 10 institutional investors expect to buy or invest in digital assets in the future.

But financial applications are just part of the hyped potential for blockchain. Boosters of the technology point to other uses such as securing medical data, tracking supply chains, facilitating votes and protecting personal-identity security.

Blockchain, however, still faces hurdles before it can be the game-changer it’s been promising to be since the 2009 debut of bitcoin.

Hash: The function that meets the encrypted demands needed to solve for a blockchain computation. Read more›››

Non-fungible token (NFT): A unique bit of data stored on a digital ledger that can be sold or traded. It can be a photo, a video or any kind of digital file. Companies such as Nike, Walt Disney, Warner Bros., the NBA and Coca-Cola are issuing NFTs.

Nodes: The computers that make up the blockchain network. They store and update records of each transaction in real time.

Smart contract: A signed, unalterable digital agreement stored on blockchain.

Token: Unit of value that can be acquired through blockchain.

Wallet: A digital wallet that lets users store or transfer digital currencies.

Central Bank Digital Currency (CBDC): A digital currency issued on a blockchain/distributed ledger technology (DLT). Governments across the globe are running pilot projects using CBDCs. A 2021 Banks for International Settlements survey found that 86 percent of the central banks worldwide are conducting research on CBDCs.‹‹‹ Read less

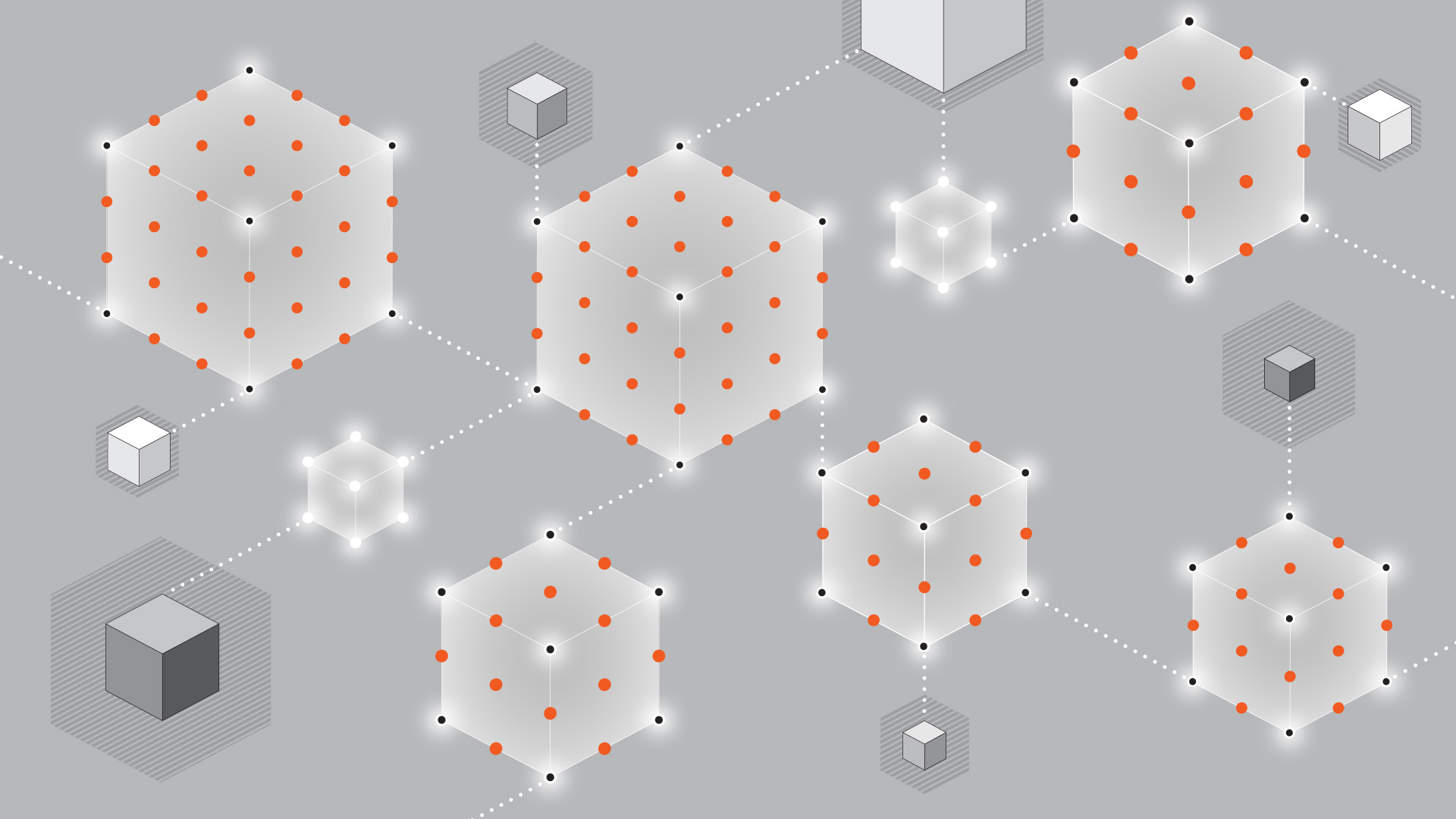

But first: What is blockchain?

But first: What is blockchain?Blockchain is a platform to store and transfer information in a way that is virtually impossible to change without other users knowing. It is secure because it is decentralized and its content is hashed. Users issue transactions to a public ledger that is managed and verified by a network of computers (called miners) without a third party such as a government, bank or other institutional intermediary getting involved.

A group of verified transactions is called a block, and the blocks are linked by complex puzzles solved by computers(“miners”) which verify the transaction and are rewarded for their efforts. Any retroactive change to the log invalidates each block that follows. The result is a certified, transparent, decentralized, tamper-proof database or ledger.

Do we really need it, though?There are difficulties on the way to blockchain world domination, however.

Perhaps the first hurdle to the Age of Blockchain, as Jesse Frederik of the Correspondent asked in 2020, is whether blockchain is a solution in search of a problem. In other words, are the problems expected to be addressed by blockchain projects better suited to solutions we already have?

But hold up, says Dragan Boscovic, research professor and co-director of the School of Computing, Informatics and Decision Systems Engineering at Arizona State University. Blockchain may need to evolve and improve, but it’s viable, solves real-world problems and is on a well-trod path to large-scale adoption.

”It is rather a common technology evolution, the same way you would upgrade from your iPhone 11 to iPhone 12 or 13,” Boscovic tells KUST Review. “There are numerous examples of blockchain technology being deployed to solve practical problems: One example is the (IBM) Food Trust solution for the food-supply chain.” (See sidebar.)

Also, says Dr. Ramesh Ramadoss, co-chair of the Institute of Electrical and Electronic Engineers’ Blockchain Initiative, it’s important to note that “blockchain” isn’t a monolith. It refers to a collection of various distributed ledger architectures. “Different architectures are used in different applications,” he tells KUST Review, “so, it’s very challenging to make a general statement about the actual usage or maturity level of the field.”

An energy gluttonAnother issue is that blockchain can have a heavy carbon footprint.

According to the Harvard Business Review, Bitcoin alone consumes around 110 terawatt hours per year – 0.55 percent of the world’s energy production. Together, Ethereum and Bitcoin annually eat up the same amount of energy as the residents of Belgium and Thailand, respectively, Digiconomist’s Ethereum Energy Consumption Index reports.

And each Bitcoin transaction, regardless of how big or small, represents $176 in electricity to power the mining, according to UK financial site MoneySuperMarket.

SOURCE: Digiconomist, World Population Review. DESIGN: Anas Albounni, KUST Review

SOURCE: Digiconomist, World Population Review. DESIGN: Anas Albounni, KUST ReviewThe technology needs the resources, but the industry is already beginning to correct itself, Boscovic says, noting “Ethereum 2.0,” which completed its long-awaited merge in September 2022. The initiative promises to reduce its energy usage by 99 percent and be “more scalable, more secure and more sustainable.”

And energy consumption for private blockchains, however, is generally not an issue, Ramadoss notes.

Still, “blockchain by its design needs to have access to a large pool of distributed resources,” ASU’s Boscovic adds. “It is from there that it is able to extract value by enabling independent validation and real-time auditing of the transactions enacted across these resources. Initial blockchain solutions made great strides in improving their scalability and throughput (e.g. speed of transaction) as well as energy efficiency. Cardano network is (another) example of new blockchain design that scales well and exhibits great energy efficiency.”

Most people think finance first when they consider the applications of blockchain. But here are seven examples of real-world uses you might not have expected. Read more›››

Food safety: The United Nations estimates that 1.4 billion tons of food are wasted every year because of supply-chain inefficiencies. The IBM Food Trust looks to change that – and control other issues, including food safety, sustainability and fraud – with its blockchain program to help supply-chain users better communicate

Avoiding spam calls: India’s telecom authority insisted that providers use digital ledger technology to solve the problem of spam calls and texts to its more than 500 million mobile-phone customers. The result? Tech Mahindra created Hyperledger Fabric, which works with all of the service providers in India to manage unwanted calls.

Entertainment: Mediachain, which was bought by Spotify in 2017, is another use of smart contracts, helping musicians agree to rates and get paid.

Health care: BurstIQ’s smart contracts help patients and doctors manage the transfer of sensitive identity information and data. Other blockchain-based systems for medical record-keeping and communication include Patientory, Immunity.Life and Medicalchain.

Marriage: Rebecca Rose and Peter Kacherginsky in April 2021 used Ethereum’s blockchain to get married. The couple, both employees of crypto-based exchange Coinbase, wrote a smart contract and exchanged “rings,” non-fungible tokens (NFTs) in the animated form of two circles merging into one.

The digital marriage was performed in conjunction with a traditional Jewish ceremony when the couple used their phones to exchange the tokens. The couple named their tokens Tabaat – the Hebrew word for ring.

Human rights: Coca-Cola, along with the US State Department and several crypto companies, is working on a plan to let workers use blockchain technology to report cases of forced labor. The initiative was announced after the Know the Chain study in 2019 found that many food and beverage companies failed to address the issue of labor abuses in their supply chains.

Tracking vaccines: With the Covid pandemic bringing vaccines and vaccine safety to the forefront of the world’s attention, IBM (again) is stepping up with a project aimed to make sure vaccines are trustworthy and distributed efficiently. IBM promises that its distribution network will ensure speed, transparency and accountability as well as the ability to monitor for adverse events and facilitate quick recalls, if needed.‹‹‹ Read less

Out of the shadowsA feature for many users is blockchain’s anonymous transactions, which is fine if you just don’t want anyone to know you’re really into collecting rare My Little Pony figurines, but it becomes a problem when that anonymity is used to launder money or for other nefarious ends.

But just because you don’t have to show ID doesn’t mean transactions are really anonymous. Identities can be tracked if you care to look hard enough, Boscovic says: “Blockchain is a rich source of digital information. With the right digital forensic tools, it is relatively easy to link a specific person to their digital identity used to transact on the blockchain.”

The FBI followed that sort of forensic trail after cyber attackers hit the Colonial Pipeline in May 2021, shutting down the American oil-pipeline system and demanding a ransom of 75 bitcoin (about $2.8 million at the time), Boscovic notes. Most of the ransom (63.7 bitcoin) was recovered; the US government in November offered a $10 million bounty for information about DarkSide, the hacking group believed to be responsible.

Of course, as law enforcement becomes more tech-savvy, users will find new ways to cover their electronic trails. The IEEE’s Ramadoss points to blockchains such as Monero and Zcash that were designed with privacy in mind and are much more difficult to trace.

Eyes on the futureSo what does a blockchain future look like? International regulation might not be a part of the puzzle. Ramadoss thinks such agreements might be extremely difficult given the fragmented nature of the global regulatory landscape.

“Crypto regulation varies from country to country,” he says. “Some countries are favorable (Singapore, El Salvador, Ukraine, Malta), some countries are working on a new regulatory framework (European Commission), and some countries outright banned cryptocurrencies (China).”

And ASU’s Boscovic sees no need for international agreements in principle. “Blockchain solutions are international and borderless by their designs,” he says. “Rather, the national regulators will need to interpret and map international blockchain business opportunities onto local business ecosystems and help their economies be competitive in such a global environment.”

Who’s in the lead?The experts disagree, however, on which regions are leading the way to a blockchain future. Ramadoss is betting on China (for non-crypto technology), which has been piloting the blockchain-based Digital Yuan project, and the European Union, whose European Commission “is funding the European Blockchain Services Infrastructure (EBSI) to serve as a single platform for issuance of identity, diplomas management, notarization of documents and trusted data sharing among the EU member states.”

SOURCE: International Data Corporation. DEDISN: Anas Albounni, KUST Review

SOURCE: International Data Corporation. DEDISN: Anas Albounni, KUST ReviewBoscovic, however, puts his money on North America. “It is primarily due to the entrepreneurial spirit of the young generation, its sharp focus on the global economy and easy access to the capital markets. Europe and Singapore are not far behind.”

But both agree that the confusing nature of the technology isn’t a problem at all. Just as most people don’t have to understand exactly why the internet works to use it, blockchain users will access the technology through user-friendly apps, they say. And the blockchain future? When will it finally arrive? “It’s already here,” Boscovic says.

Get the latest articles, news and other updates from Khalifa University Science and Tech Review magazine